CIM Market Commentary | Opportunities and Risks in The New Year

The year 2024 proved to be quite volatile for fixed income investors, as yields fell dramatically from their heights in 2023, then rose again in the fourth quarter (Q4), closing the year within a stone’s throw of the highest levels of the year. The rise in yields in Q4 was due, in large part, to uncertainty surrounding what a Trump presidency could mean for inflation and the economy. We also saw equity markets reach valuation levels that are among the highest in recorded history. In light of these extraordinary market conditions, we have provided a list below of the most important factors we believe municipal bond investors should consider as they seek to navigate this uncertainty over the next twelve months.

- Broader municipal sector credit fundamentals remain steady

- Substantial reserve balances amplified by unprecedented federal pandemic aid buffer against potential revenue disruption

- Municipal sector is highly rated with positive ratings momentum since the onset of the pandemic

- Upgrade-to-downgrade ratios have been strongly positive for 14-15 consecutive quarters through Q3 2024*

- Municipal bond default rates remain well below 1% compared with 2.6% for corporates**

- Vast majority of municipal defaults are unrated credits (approximately 87%***), a striking contrast to corporate defaults

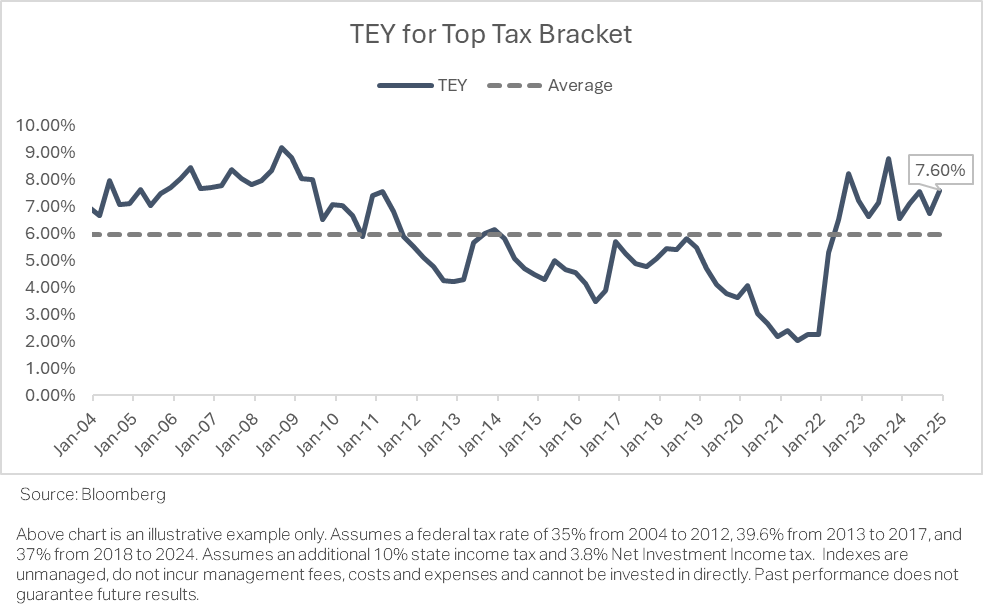

- Absolute municipal bond yields are compelling, particularly for investors in higher tax brackets. See chart below

- For the month of December 2024, municipal bond yields rose sharply, albeit by a smaller magnitude than Treasuries:

- The 10-year Treasury yield rose to 4.57% from 4.19%, or 38 basis points. The 10-year ‘AAA’ municipal bond yield moved to 3.04% from 2.76%, cheapening by 28 basis points. The 30-year MMD ‘AAA’ municipal bond yield moved to 3.90% from 3.59%, or 31 basis points

- The 10-year municipal-to-treasury ratio was essentially unchanged. It started the month at 65.8% and moved to 66.7% using a federal tax rate of 39.6%

- According to JP Morgan, Bloomberg’s Investment Grade Tax-Exempt Municipal Index recorded a total return of -1.46% in December, culminating in a full-year return of 1.05% for 2024. This full-year performance outpaced the UST Index (+0.58%)

- 2024 inflows into municipal bond funds were nearly $42 billion reflective of strong investor demand given yield, tax advantages, and diversification needs****

- Municipal new-issue total supply was a record-high $504 billion in 2024. Supply is expected to remain solid in 2025, presenting a diverse investment opportunity set ****

- December’s Personal Consumption Expenditures (PCE) Price Index, commonly referred to as core PCE, the Federal Reserve’s preferred measure of price changes, was below market consensus expectations (core PCE rose 2.8% year-over-year versus an expected 2.9%, while headline PCE inflation year-to-year was 2.4% versus an expected 2.5%). Continued moderating inflation should be favorable for the longer-term interest rate trajectory and fixed income investors

Data sources:

*JP Morgan

**S&P: “2023 Annual U.S. Corporate Default And Rating Transition Study”

***Charles Schwab

****LSEG Lipper data

Please remember that past performance may not be indicative of future results. Net-of-fee performance returns are calculated by deducting the actual Clinton Investment Management, LLC investment management fee from the gross returns. Performance returns include the reinvestment of income and capital gains. Actual results may differ from the composite results depending upon the size of the account, investment objectives, guidelines and restrictions, inception of the account and other factors. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available upon request.

The views and opinions expressed are not necessarily those of the distributing firm or any affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent your firm’s policies, procedures, rules, and guidelines.