CIM Market Commentary | Cutting Interest Rates is a Process

- When the Fed begins to cut interest rates, next month, as markets now expect, it will likely be the first of a series of cuts, rather an isolated event.

- The extremely weak July payroll report triggered the Sahm Rule for the first time since the previous recession. The Sahm Rule is a statistical measure that has historically indicated when the US economy has entered recession. This condition has been correlated with recession 100% of the time, since 1970.

- The first rate cut of an easing cycle will likely have the opposite effect of its intended purpose, that is the first cut will result in a “tightening” of financial conditions rather than an easing.

- The outlook for fixed income investors, and municipal bond holders in particular, has improved meaningfully in recent weeks.

- The best opportunities to achieve extremely attractive risk-adjusted returns, for individuals in the highest tax brackets, remain in the municipal bond market, in our view.

- Whether moving from cash to maximize tax-free cash flow, or extending duration to capture greater total return as rates fall, the case for acting before the next leg down in rates begins, is an extremely compelling one, in our view.

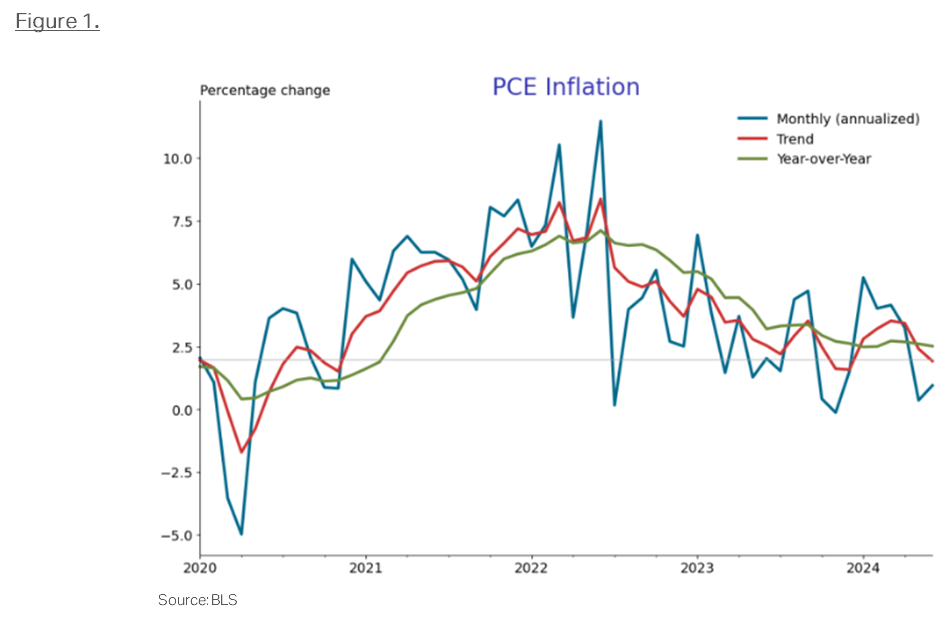

Federal Reserve Chairman Powell stated, during his July Federal Open Market Committee press conference, that cutting interest rates is a process. This is extremely important as it implies that when the Fed begins to cut interest rates, next month, as markets now expect, it will likely be the first of a series of cuts, rather an isolated event. While many strategists and media pundits, throughout 2024, have posited that further rate “hikes” might be necessary, or at the very least, interest rates would need to stay “higher for longer,” we at Clinton Investment Management (CIM) have held firm to the view that rate cuts would begin in earnest very soon. Our conviction remains high due to the downward direction of a variety of economic indicators we closely follow. These include domestic and global inflation, weakening consumer spending, US economic activity, and rising unemployment over the past three months, just to name a few. The recent weak payroll data, together with falling consumer prices, reflected in the Fed’s preferred measure of inflation, Personal Consumption Expenditures (PCE), see Figure 1, appear to be indicating that the US economy is approaching an inflection point. The Treasury market reflects this reality and has priced in a near 100% likelihood that the Fed will begin cutting interest rates, as soon as September, to ease financial conditions to arrest the decline in economic activity that has begun.

The extremely weak July payroll report also triggered the Sahm Rule for the first time since the previous recession. The Sahm Rule is a statistical measure that has historically indicated when the US economy has entered recession. The rule identifies the inflection point at which the US unemployment rate rises by at least 0.5%, from its 12-month low, over the prior three months. This condition has been correlated with recession 100% of the time, since 1970. When Powell was asked specifically about the triggering of the Sahm Rule, in his July press conference, he attempted to allay concerns about recession, while at the same time describing the Sahm Rule as a “statistical regularity”. This characterization implies it is a reasonable expectation that this economic indicator will, once again, be accurate.

What should investors do with this new information? When considering likely outcomes over the next 12 to 18 months, we are reminded that the first rate cut of an easing cycle will likely have the opposite effect of its intended purpose, that is the first cut will result in a “tightening” of financial conditions rather than an easing. The reason for this seemingly contradictory outcome rests in the notion that the first cut is an extremely powerful signal to market participants and borrowers alike. The first cut is a unique and extraordinary statement to corporations, home buyers, car buyers, commercial property investors, and borrowers of all shapes and sizes, that the first cut is likely to be one of many. Once the cut is made, informed borrowers understandably conclude that future cuts will be forthcoming and, therefore, delay their borrowing needs in the hopes of achieving lower borrowing costs in the future. Incentivizing borrowers, corporations, and individuals to wait until lending and financial conditions ease or improve further, causes loan demand to fall, results in a cascading effect, triggering a further contraction in economic activity. This forces the Fed to cut more deeply to incentivize borrowers off the sidelines. This is why the Fed has been forced to reduce interest rates below the neutral rate of interest, R*, during prior recessions and easing cycles.

The notion of an economic soft-landing as the most likely outcome, whereby the economy avoids recession, is an unlikely outcome, in our view, especially when one considers the entirety of historical US economic outcomes and monetary policy. A soft landing has only been achieved on one occasion in history. In 1995 Fed Chairman Greenspan proactively cut interest rates as inflation fell. In contrast, Powell and this Fed have kept interest rates at the highest levels for almost a year, even as inflation has fallen by almost 80%. The Fed hasn’t even stopped winding down its balance sheet through Quantitative Tightening (QT). The Fed is tightening financial conditions each day it waits to act. Therefore, it is hard to see how the US economy escapes recession this cycle. We are sorry to say that this time is not likely to be different than cycles of the past, regardless of how much we may hope that was not the case.

Therefore, the outlook for fixed income investors, and municipal bond holders in particular, has improved meaningfully in recent weeks. Inflation continues to fall as evidenced by further declines in the Consumer Price Index (CPI), Producer Price Indices (PPI), as well as the Fed’s preferred measure of inflation, PCE. The softening of economic projections has caused long-term interest rates to fall meaningfully. Since the peak in interest rates in October of 2023, Treasury yields have declined by over 1.10% or 110 basis points. For investors who were waiting to see if rates would stop rising, we can say with confidence that that moment has passed.

As our clients and readers know, we have been recommending, for some time, that investors prepare for lower rates by proactively locking in higher yields in longer-term bonds, before rates fall further. Doing so would provide higher cash flow for investors as short-term rates decline, as the Fed embarks on the next easing cycle, while longer-duration securities can be expected to deliver higher total rates of return over time. In general, investors who followed this advice over the past year have been rewarded as bond prices have risen while rates fell. Investors who may have chosen to wait to act can take comfort as rates have much further to fall, in our view.

Chair Powell stated in his recent press conference, assuming economic data continues on its downward path, the Fed will begin “normalizing” interest rates very soon. The question remains. What does interest rate normalization look like? We are pleased to share that the Fed has already told us what to expect. The normalized level of the Fed Funds rate, that is neither expansionary or contractionary, better known as the Fed’s neutral rate or R*, is somewhere between 2.00% and 2.75%. Given that the Fed Funds rate is currently 5.25%-5.5%, this means the Fed is likely to cut interest rates by over -200 to -300 basis points before the end of the easing cycle. This outcome is not priced into bond yields or prices at present, in our view, which means bonds are attractively valued. We are, therefore, compelling investors to move deliberately, in the near term, to extend out of cash instruments and short-duration bonds, before those yields fall further, as they are likely to, in the coming weeks and months. The level of reinvestment rate risk in cash and preferred savings/money market instruments is now the highest it’s been since prior to the global pandemic.

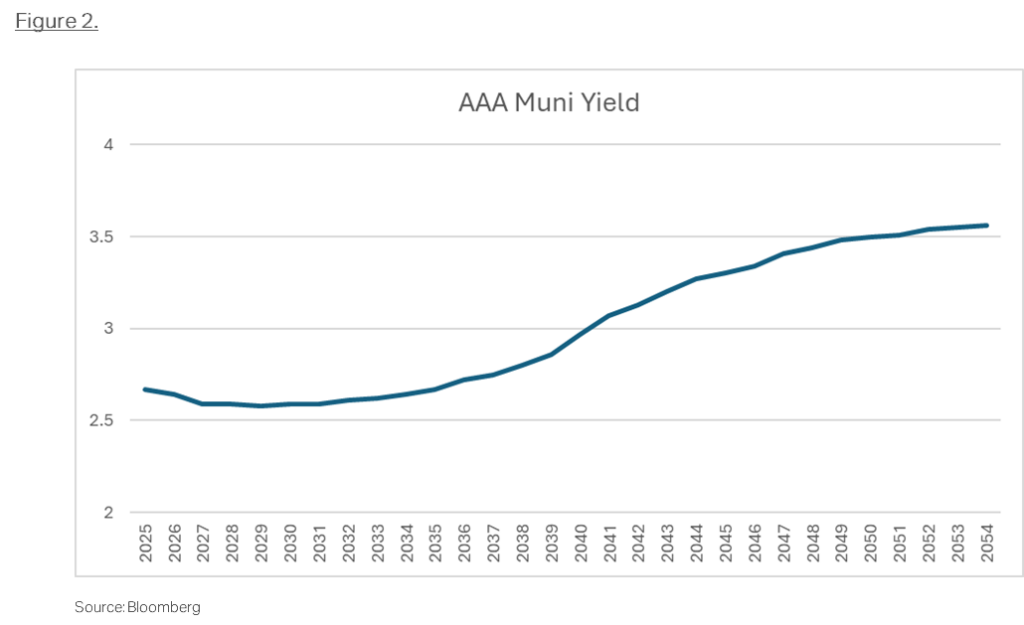

The best opportunities to achieve extremely attractive risk-adjusted returns, for individuals in the highest tax brackets, remain in the municipal bond market, in our view. While the short end of the muni curve remains inverted, see Figure 2, the long end of the curve remains steeply sloped, providing investors with the opportunity to both increase yield and extend duration, to take advantage of the falling interest rate environment we expect going forward.

Municipal credit quality remains stable, while upgrades continue to outnumber downgrades by a healthy margin, providing confidence that municipal credit quality should remain stable even in the face of slowing US economic growth. Even if the upgrade to downgrade ratio weakens from current levels, the municipal bond default rate is extremely low, even during downturns. Corporate bond default rates are materially higher across all rating buckets. Municipal bonds continue to offer attractive returns from yield alone, with substantially lower risk/standard deviation of returns as compared to the broader equity markets. Therefore, given our outlook, we believe the total return opportunity in longer intermediate and longer duration municipal bonds is particularly compelling, over the next 12 to 24 months.

As we approach the back half of the year, we firmly believe the best of days for this business cycle are behind us. Whether the US economy is already in recession, as the Sahm Rule indicates, or the economy enters recession in the months ahead is not our greatest concern. More concerning is the knowledge that many investors are largely unprepared for what is likely to come next. The high levels of reinvestment rate risk embedded in cash and cash-like instruments, whose yields are likely to fall precipitously going forward, offer little compensation to investors who delay action. We firmly believe that this is not the moment to be complacent. We have seen, in the prior weeks and months, just how quickly interest rates can fall. While it took months, if not years, for rates to rise to their current levels, we know that, at times, rates can fall dramatically in a matter of seconds, when the market eventually perceives that the current business cycle has officially ended. This is why we are encouraging investors to be proactive. Whether moving from cash to maximize tax-free cash flow, or extending duration to capture greater total return as rates fall, the case for acting before the next leg down in rates begins, is an extremely compelling one, in our view.

Clinton Investment Management Update

We want to take this moment to sincerely thank our clients, advisors, and the institutions we serve, for their ongoing trust and loyalty. We are extremely proud and grateful that our municipal bond strategies have continued to deliver meaningful value to the clients and institutions over time. CIM has grown meaningfully over the past 12 months, as we made strategic investments in our team and continue to enhance our firm’s operational infrastructure. While we are enjoying our best year of growth since our firm’s founding, we are equally proud of our ability to attract and retain extremely talented and experienced professionals, at all levels of the firm. We are confident our expanded team will enhance and guide our firm’s growth, as well as our strategies, in the years ahead. We are deeply grateful for the trust that our clients have placed in us, which is evident in the growth of our assets under management (AUM). Our AUM are now approaching $3.5 billion, rising by over 100% since the end of 2022. Our differentiated Municipal Credit Opportunities strategy is now our firm’s largest strategy with AUM exceeding $2 billion, while our Market Duration strategy AUM has grown in excess of $1 billion.

Please do not hesitate to reach out to us with any questions regarding the differentiated strategies we offer or where we are seeing the best market opportunities going forward.

Best Regards,

Andrew Clinton

CEO

.

Please remember that past performance may not be indicative of future results. Net-of-fee performance returns are calculated by deducting the actual Clinton Investment Management, LLC investment management fee from the gross returns. Performance returns include the reinvestment of income and capital gains. Actual results may differ from the composite results depending upon the size of the account, investment objectives, guidelines and restrictions, inception of the account and other factors. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available upon request.

The views and opinions expressed are not necessarily those of the distributing firm or any affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent your firm’s policies, procedures, rules, and guidelines.