CIM February ‘25 Market Commentary | Three Dimensional Chess

- Investors in financial markets today are playing a different game altogether, as the rules of the game appear to change by the minute or, shall we say, by the tweet

- If one were looking for a bull market, look no further than the bull market in uncertainty

- The President has the authority to increase tariffs on goods/raw materials, not services. Goods represent less than 6% of US GDP

- With a high degree of conviction, we believe the tax-exempt nature of the municipal bond market will be preserved

- We are reminded that income is the most important contributor to one’s total return over time. A yield of over 4% tax free equates to over 7% return on a taxable equivalent basis, for someone in the highest tax bracket. There are very few, if any, investment alternatives that offer a similar return potential, with the same or lower risk

- The relatively low risk of municipals, as compared to other historically riskier asset classes, together with the attractive tax-free cash flow they now provide, are a compelling option for investors looking to increase their cash flow while they await greater clarity to what the future may bring

Even the most casual of chess players is aware that, in its simplest form, chess requires careful assessment of an opponent’s strengths and weaknesses and serious consideration of a multitude of tactics, ranging from aggressive to defensive. Risks must be measured together with the expected reactions of an opponent to the movement of varied game pieces, all while playing on a two-dimensional game surface. For those who have attempted to play three-dimensional chess, the complexity of the game is exponentially more challenging, as players are required to consider strategy and movement on multiple surfaces, at varying heights and depths. Investors in financial markets today are playing a different game altogether, as the rules of the game appear to change by the minute or, shall we say, by the tweet. The Federal Reserve cut the Federal Funds rate by 0.50%, or 50 basis points in September. Yet, for the first time in history, Treasury yields rose by 1.00%, or 100 basis points, over the following three months. Chairman Powell could not have been clearer in his press conference in September, when he stated that the Fed was “recalibrating” its focus away from inflation and toward supporting the jobs market. The Fed had made substantial progress toward its 2% inflation goal and was expecting a further decline in inflation, over time, albeit on a bumpy path. However, investors did not respond to the Fed’s actions or statements, as they appeared distracted by the constant barrage of news headlines surrounding the Presidential election. Who can blame investors for this distraction considering that it has taken up all the oxygen in the room for many months, the result being a material increase in stock and bond market volatility, since September. Investors are understandably struggling to assess the potential impact that tariffs and a possible tax cut extension could have on inflation and the broader economy. Fear has captured investor imaginations, triggering visions of runaway inflation that could result in dire interest rate outcomes. Investors have been forced to navigate headlines crafted to instill just those kinds of fears. Like three-dimensional chess, investors are being forced to consider possible scenarios and outcomes, with imperfect information, which, in many cases are unknowable, without the benefit of time. If one were looking for a bull market. Look no further than the bull market in uncertainty.

It is important to note that President Trump used tariffs extensively during his first term. However, few appear to remember that inflation was lower when Trump left office than we he arrived. We also now see, as was the case in recent negotiations with Mexico and Canda, Trump clearly intends to use tariffs for leverage in trade negotiations. When we consider the potential impact of tariffs, even on the largest scale, the President has the authority to increase tariffs on goods/raw materials, not services. Goods represent less than 6% of US GDP. Therefore, even in the event that tariffs are implemented broadly, which, despite the rhetoric, now appears less likely, the inflationary and economic impacts would likely be limited and ephemeral, in our view.

We must also consider the positive, yet fleeting, economic impact of the Tax Cut and Jobs Act (TCJA) during Trump’s first term. While it was not that long ago, it appears that some have forgotten that the US economy slowed considerably during the last year of President Trump’s first term, even prior to the Covid onset. While some have claimed an “unleashing” of the US economy could occur in Trump’s second term, due to the extension of the TCJA and a more pro-business posture, in our view, too little consideration has been given to the notion that, during Trump’s first Term, taxes were higher when he took office. Therefore, when tax rates fell there was a resulting, albeit temporary, positive economic impact?. This time is different. Tax rates have already been reduced. The most likely outcome is simply an extension of the existing tax regime where the immediate economic benefit is likely to be muted. Another important consideration is that the Trump administration will need to use budget reconciliation to extend the JCTA, meaning that he will need to “create” revenue to offset lost revenue from the extension of tax cuts. We see Trump already acting on this promise, through the Department of Government Efficiency (DOGE), as he seeks to reduce the size of government and government expenditures via the elimination, of what the administration has deemed, waste and fraud. If the President is successful, the resulting impact will be higher joblessness, as government employees are laid off, resulting in reduced consumption, and lower tax collections for state and local governments. This will have a chilling effect on the broader economic growth, in our view.

What does this all mean for municipal bond investors? One of the roughly 100 tax preference items the administration has listed as a potential source of revenue, to extend the TCJA, is the repeal of the tax exemption on municipal bonds. This has caused a significant degree of concern for municipal bond investors. However, this notion has been floated many times over the past 30 years. Each time the resulting outcome is very little to no change in the municipal tax exemption. While we never like to hear that the tax-exemption of munis is being threatened, it is important to note that any change to the outstanding bonds would be highly unlikely as it would be arguably unconstitutional to do so retroactively and would, no doubt, be vigorously challenged in the courts. In the scenario where the tax-exemption on munis is removed for all new issues, any outstanding tax-free bonds would remain as such, making them highly desirable. Given the finite nature of supply and an increased demand, we would expect outstanding bonds to perform quite well. While private activity and select higher education institutions may be exposed to this risk, we believe the broader municipal market will remain unscathed. With a high degree of conviction, we believe the tax-exempt nature of the municipal bond market will be preserved.

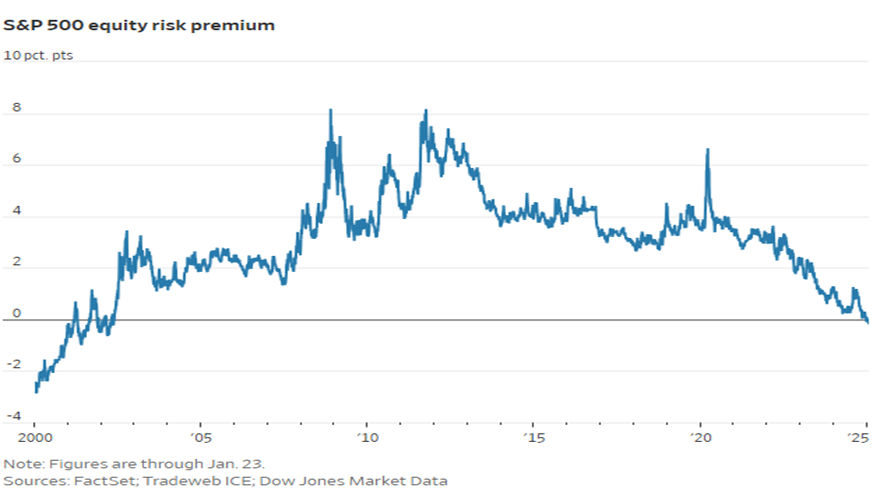

As we consider that path forward for municipal fixed income investors, we are reminded that income is the most important contributor to one’s total return over time. A yield of over 4% tax free equates to over 7% return on a taxable equivalent basis*, for those in the highest tax bracket. There are very few, if any, investment alternatives that offer a similar return potential with the same or lower risk. For example, the current Equity Risk Premium (ERP), the premium equity investors should be paid for the higher risk of holding public equities, is now negative compared to US Treasury bonds for the first time since the early 2000’s, see Figure 1.

Throughout history, when the ERP has been negative, equity prices have fallen meaningfully. While that is not to say equity prices will fall anytime soon, it simply means the risks have risen and investors are not being compensated for that risk, in our view. Therefore, we believe that municipal bonds are well positioned given the substantial income one can generate and retain on an after-tax basis.

Credit quality in the municipal bond market remains stable and we expect that to persist going forward. According to Morningstar+, investors are currently the most overweight stocks and underweight bonds they have been in over ten years. When one also considers that yields on preferred savings accounts and cash instruments have declined materially, since the Fed began cutting rates, those that are heavily exposed to cash and short duration instruments should be compelled to begin extending out of cash, given the steep slope of the municipal curve.

As we consider the many dimensions of the broader marketplace, it is clear investors have imperfect information from which to draw firm conclusions and plan their next move. The only thing we know with certainty, is that the outlook is uncertain. In these moments, the relatively low risk of municipals, as compared to other historically riskier asset classes, together with the attractive tax-free cash flow they now provide, are a compelling option for investors looking to increase their cash flow while they await greater clarity as to what the future may bring.

Clinton Investment Management 2024 Firm Update

We would like to take a moment to express our sincerest thanks to the advisors and clients with whom we partner. Last year was another strong year of growth and relative performance for our firm and our strategies. We added staff, new investment capabilities, expanded our offices to our new location in downtown Stamford, while achieving our strongest year of asset growth in our firm’s history. Over $1.3 billion in new client contributions were committed to our clearly differentiated investment strategies in 2024. I would like to take this opportunity to recognize our extraordinary team who worked tirelessly, throughout the year, to achieve these important milestones. Most importantly, we know that our success would not be possible without the ongoing trust, confidence, and loyalty of our client’s and advisor partnerships, for which we are deeply grateful. We remain steadfast in our commitment to consistently delivering meaningful value to our clients over the long term and we look forward to another strong year in 2025.

If you should have any questions regarding this commentary or the municipal bond market more broadly, please do not hesitate to contact us directly.

Best Regards,

Andrew Clinton

CEO

*The taxable equivalent yield is calculated by dividing the tax-exempt yield by 1- the maximum federal income tax rate of 40.8% (37% federal + 3.8% Medicare tax).

+Jan 22, 2025 Jeffrey Ptak Morningstar How Far Out-of-Whack Are Fund Investors’ Asset Allocations? $800 Billion, Give or Take https://www.morningstar.com/portfolios/how-far-out-of-whack-are-fund-investors-asset-allocations-800-billion-give-or-take

Please remember that past performance may not be indicative of future results. Net-of-fee performance returns are calculated by deducting the actual Clinton Investment Management, LLC investment management fee from the gross returns. Performance returns include the reinvestment of income and capital gains. Actual results may differ from the composite results depending upon the size of the account, investment objectives, guidelines and restrictions, inception of the account and other factors. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available upon request.

The views and opinions expressed are not necessarily those of the distributing firm or any affiliates. Nothing discussed or suggested should be construed as permission to supersede or circumvent your firm’s policies, procedures, rules, and guidelines.