What just happened?

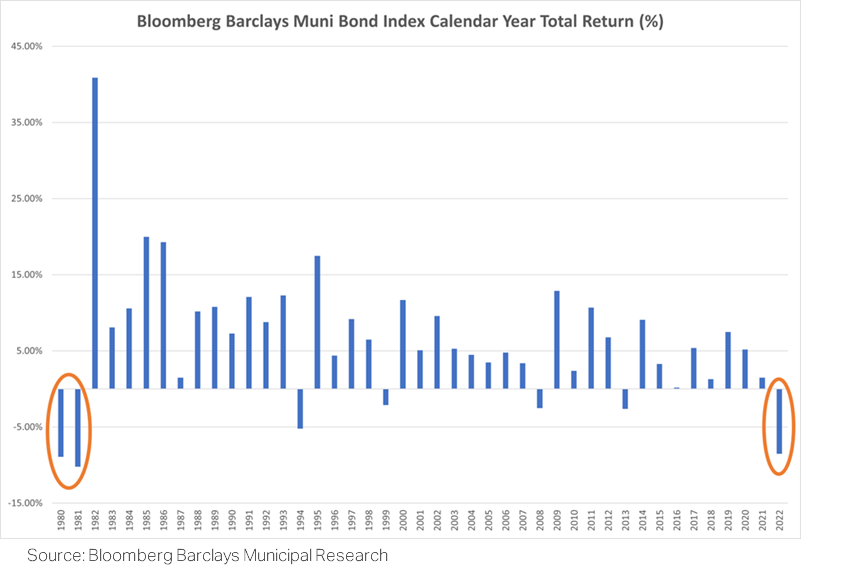

In November fixed income markets and municipal bonds in particular experienced the best monthly return since 19821. Clinton Investment Management’s Market Duration and Municipal Credit Opportunities strategies enjoyed their best monthly performance in our firm’s history2. Positive bond market momentum has carried into December as well.

Where are rates headed?

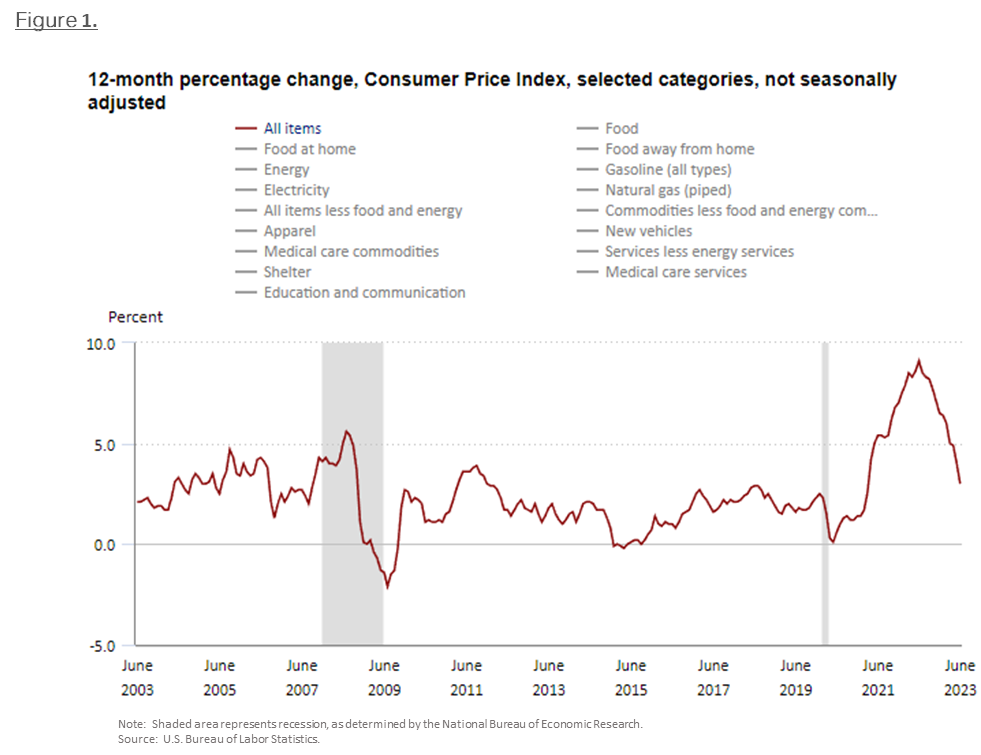

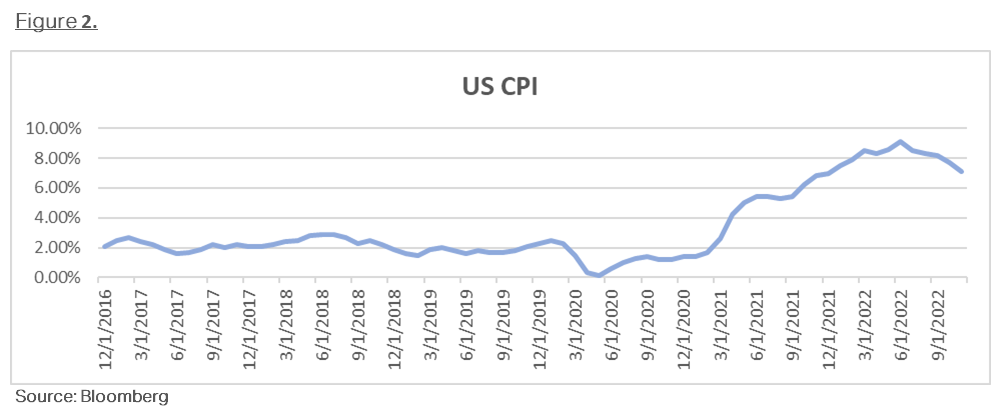

- Five consecutive months of declining durable goods prices, including furniture, used cars and appliances is evidence of deflation. Airfares are down over 15% year-over-year according to the most recent CPI data.

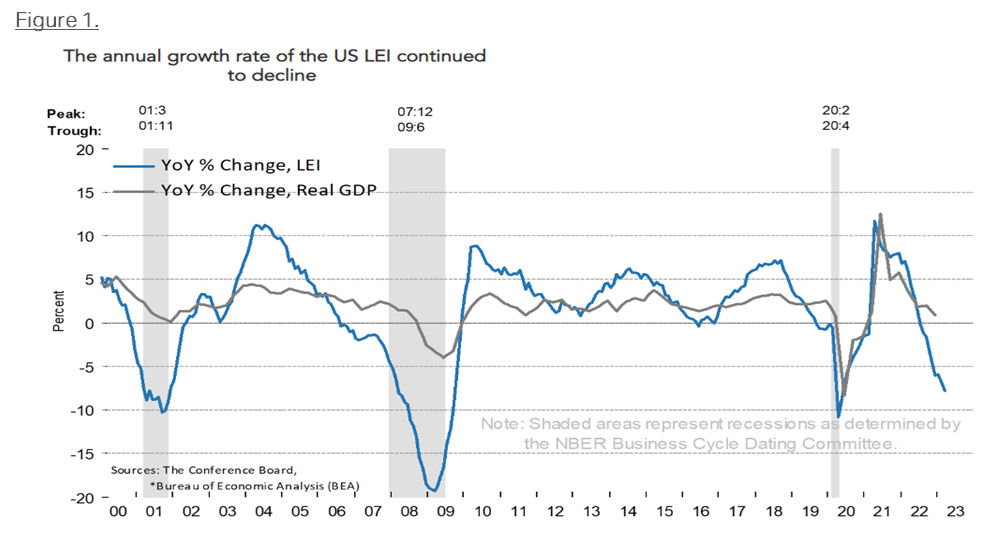

- 20 consecutive months of declining leading economic indicators have historically been correlated with recession 100% of the time.

- Declines in inflation to the degree we have seen have been historically correlated with recession 100% of the time.

- Increases in joblessness to the degree the Fed is forecasting has been historically correlated with recession 100% of the time.

- Oil is in a bear market, down over 20% from its high in September despite OPEC supply cuts and war in the Middle East.

- CPI 3.2%, ex lagging shelter, is actually 1.5%-1.8% today…Rosenberg Research believes inflation could be 0% by the end of 2024.

- Fed historically cuts rates 10 months following Fed pause on average, interest rates move prior to cuts.

- Walmart has stated that its outlook for the food and goods industry is heading into a period of deflation.

- The Fed has historically cut 500 bps, on average, during prior easing cycles.

What should investors do now?

Act expeditiously, as it is better to be early rather than late to reduce the risk of missing further declines in rates.

Where are the best opportunities in Munis today?

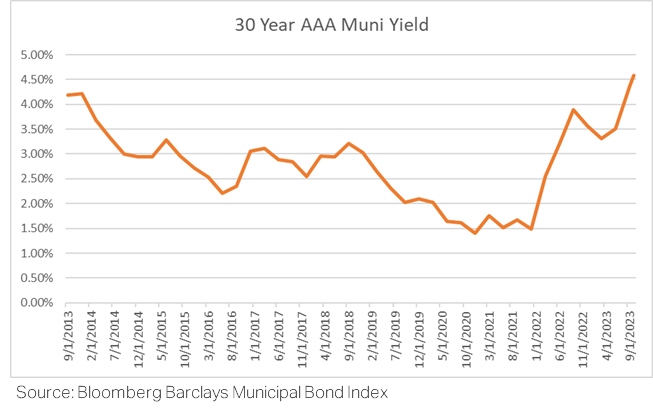

The muni curve is positively sloped by 0.83% or 83 basis points 2s/30s while the muni curve is inverted by -26bps 2’s/10’s, a dislocation from the inverted Treasury curve and an indication of the relative richness and likelihood of future underperformance of short-intermediate maturities in the muni market.

Moody’s municipal default study demonstrates the higher risk-adjusted yield/return in lower investment grade bonds presents opportunity to investors with longer-term investment horizons, seeking to maximize tax-free cash flow and total return over time.

There may be a significant opportunity to increase portfolio tax efficiency through active tax loss/gain harvesting strategies heading into 2024 remains.

Endnotes

Clinton Investment Management, LLC (“CIM”) is registered as an investment adviser with the US Securities and Exchange Commission under the Investment Adviser’s Act of 1940. CIM headquarters is located at 201 Broad Street, 8th Floor, Stamford, CT 06901.

Please refer to clintoninvestment.com for CIM’s most recent performance data.

Data referenced may have been obtained from a variety of sources sources, including, but not limited to, Bloomberg, CreditScope or other systems and programs. CIM makes no representation concerning the accuracy of information received from any third party.

Past performance may not be indicative of future results. There can be no assurance that the future performance of any specific investment, investment strategy, or product, made reference to directly or indirectly in this market brief, will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. The information contained herein is not intended as an offer or solicitation for the purchase or sale of any securities. High grade and high yield securities which may be mentioned herein may not be suitable for all investors. A credit rating of a security is not a recommendation to buy, sell or hold securities and may be subject to revisions, including reductions or withdrawals, at any time by the rating agency.

Interest on municipal bonds is generally exempt from federal taxation and may also be free of state and local taxes for investors residing in the state and/or locality where the bonds were issued. However, some municipal bonds may be subject to federal alternative minimum tax (AMT). Municipal bonds are subject to capital gain or losses if they are sold prior to maturity.

There is no assurance any of the market trends or forecasts mentioned will continue or occur and any estimates or opinions offered are subject to change without notice. Any statements pertaining to market trends are based on current market conditions and any future market conditions will always remain uncertain. You should not assume that any discussion or information contained in this market brief serves as the receipt of, or as a substitute for, personalized investment advice and you should therefore consult with an investment professional before making any investment using the content, either express or implied, of the information provided. This information should not replace your consultation with a financial professional regarding your tax situation. CIM is not a tax advisor.

A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product, made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Please consult with an investment professional before making any investment using content or implied content from any investment manager. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.